AI and Cloud Economics in Regulated Industries: Governing the Spend You Cannot See

95% of GenAI pilots return nothing measurable, yet regulated industries are scaling AI fastest under the heaviest constraints. Why sovereignty and attribution now decide ROI.

Regulated industries are scaling AI faster than anyone — under constraints no one else faces. They are now the primary buyers of sovereign cloud capacity after governments, yet 95% of generative AI pilots return nothing measurable on the P&L, and a bank cannot send its cost data to a third-party tool to find out why.

That is the defining economic problem of AI in 2026 for any organisation operating under supervision. The spend is enormous and growing. The governance architecture available to most enterprises is structurally unavailable to a regulated one. And the people who must defend AI investment — to a board, to an auditor, to a supervisor — are being asked to prove a return on workloads they cannot fully see.

This briefing is for the CFO, Head of FinOps, and CTO carrying that question. It explains why AI breaks the cloud economics of regulated industries specifically, what three constraints make the problem unique, and how to govern AI spend without exporting a single billing record from your environment.

Executive Summary

- AI spend is now a board-level question, not an IT line. Only 28% of AI projects deliver ROI (Gartner, 2026), and 95% of generative AI pilots produced zero measurable P&L return (MIT Project NANDA, 2025). Every failed pilot still generates a bill.

- Cloud waste is rising again because of AI. After five years of decline, cloud waste climbed to 29% in 2026 — roughly $182B globally — attributed directly to the complexity of AI workloads (Flexera, 2026).

- Regulated industries cannot use standard tooling. Sovereign cloud IaaS spending will reach $80B in 2026, with regulated industries and critical infrastructure named as the primary buyers after governments (Gartner, February 2026). SaaS-only cost tools that export billing data are disqualified by data-residency rules.

- Governance has become a strategic differentiator. 54% of IT leaders now rank AI governance among their top enterprise risks, up from 29% two years earlier.

- The fix is architectural. Govern AI cloud economics with a FinOps control layer that runs inside the regulated perimeter, normalises every cost source onto the open FOCUS specification, and attributes AI spend to the business unit that consumed it — without data egress.

Why AI Breaks the Cloud Economics of Regulated Industries {#why-ai-breaks-cloud-economics}

AI spend behaves differently from every cost category that came before it, and the difference is what makes it ungovernable with the tools most enterprises already own. Traditional cloud cost is broadly linear and predictable: an instance runs, it bills by the hour, and rightsizing recovers the obvious waste. AI cost is spiky, non-linear, and detached from value. A model that trains for twice as long does not return twice the business outcome, but it does produce twice the bill.

The scale of the shift is unambiguous. AI management has become nearly universal among FinOps teams at 98%, up from 63% the prior year — the fastest scope expansion the FinOps Foundation has ever recorded across its 1,192-respondent survey representing more than $83B in annual cloud spend. Cost management has spread well beyond infrastructure as enterprises work to bring AI spending under control.

The trouble is that the spend is outpacing the visibility. Roughly 72% of organisations use generative AI cloud services, but only 63% of FinOps practitioners track AI spend at all — meaning a third of the organisations spending on AI have no systematic view of what those services cost. That gap is the mechanism behind the rise in waste. Idle GPU instances, orphaned inference endpoints left running after an experiment ends, and silently accumulating vector stores convert directly into the 29% waste figure Flexera reported for 2026, the first increase after five consecutive years of decline.

Now add the regulated context. A bank, insurer, healthcare provider, or government body is scaling AI under the same non-linear cost dynamics — but with three additional constraints that change what governance even means.

The Three Constraints That Don’t Apply Anywhere Else {#three-constraints-regulated}

The reason regulated AI economics is a distinct discipline, rather than a harder version of the same problem, comes down to three constraints that a SaaS company or retailer simply does not carry.

Data sovereignty makes the obvious tooling unavailable. Cost and usage telemetry in a regulated environment is itself sensitive: it reveals which models run, on what data, at what volume, and for which clients. Exporting that to a third-party multi-tenant SaaS platform — which is how most cloud cost tools work — creates a data-residency exposure that compliance functions will not sign off. This is the same force driving the sovereign cloud market to $80B in 2026, and the reason financial services institutions are increasingly self-hosting open-weight models rather than calling external APIs. As practitioners at recent industry sessions put it plainly: when your trading strategies, M&A documents, and client portfolios are the data, sending them to a shared platform is a non-starter — and that logic applies to the cost data describing those workloads just as much as to the workloads themselves.

Attribution must survive an audit. In an unregulated business, “good enough” cost allocation is good enough. In a supervised one, attribution is evidence. When a regulator or internal audit function asks which AI workloads are productive, what each costs, and who consumed them, the answer cannot be a dashboard estimate — it must be a traceable, defensible figure tied to a business unit. Tagging hygiene that leaks 20% of spend into an “unallocated” bucket is not a reporting inconvenience here; it is a control gap.

ROI must be defensible, not merely positive. A board can be told that AI saved money. A supervised board must be shown the working. With only 28% of AI projects delivering ROI and 95% of pilots returning nothing measurable, the regulated CFO is in the hardest position of all: required to fund AI to stay competitive, required to prove the return, and forbidden from using the easiest tools to measure it. The 78% of FinOps teams now reporting to a CTO or CIO — up from 61% in 2023 — is the organisational signal that this accountability has arrived at the top of the house.

These three constraints compound. Each one individually rules out a class of solution. Together they define a requirement that very few platforms were built to meet.

What Is AI Unit Economics in a Regulated Context? {#what-is-ai-unit-economics}

AI Unit Economics is the discipline of attributing the full delivered cost of an AI workload — inference tokens, GPU compute, vector storage, data-platform processing, and orchestration overhead — to a defined unit of business value such as a product, customer, model, or transaction. Where traditional cloud cost allocation distributes infrastructure spend by resource tag, AI Unit Economics measures cost against value, exposing whether a given AI capability is profitable on a per-use basis.

The regulated distinction is the standard of proof. Elsewhere, unit economics is a useful management lens. In a supervised institution it is the financial control layer that converts opaque GPU and token spend into evidence a CFO can stand behind — to a board, an auditor, or a supervisory authority. It answers the question that cost optimisation never can: not “how do we spend less on AI?” but “what does one unit of this AI capability cost, and is it worth more than that?”

This is why optimisation alone is insufficient for a regulated estate. Rightsizing GPUs and improving commitment coverage reduces the bill, which matters. But a board cannot defend AI investment on reduced waste alone — it has to show that AI value exceeds fully loaded delivery cost, per unit, with attribution that holds up under scrutiny. AI Unit Economics is the bridge from “we control our AI spend” to “we can prove our AI spend was justified.”

The Architecture Problem: You Cannot Govern What You Cannot See {#architecture-problem}

Every regulated AI governance failure traces back to the same architectural mismatch: the data lives where it must, and the tools want it somewhere else.

A standard SaaS cost platform pulls your billing and usage data into the vendor’s cloud, processes it there, and returns analysis. For an unregulated company that is a convenience. For a regulated one it is the disqualifying step, because the export itself is the compliance event. The result is a familiar and damaging compromise: either the institution forgoes proper AI cost governance entirely, or it runs two disconnected systems — one for the cloud the tools can reach, and a manual, spreadsheet-driven effort for everything the tools cannot.

The architecture that resolves this inverts the data flow. Rather than exporting cost data to the platform, the platform’s collector runs inside the customer’s own perimeter and the data never leaves. DigiUsher implements this through its Secure Relay Proxy — a Bring Your Own Cloud (BYOC) model where reading, normalisation, and attribution all happen within the regulated environment. It is the architecture behind DigiUsher’s deployment at institutional scale at a large Bank, where data sovereignty was the precondition for any FinOps platform at all.

The coverage required is the full technology cost surface, normalised onto one specification:

DigiUsher FinOps OS — Regulated AI Cost Surface (FOCUS 1.x Native)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

┌──────────────────────────────────────────────────────────┐

│ DigiUsher FinOps OS │

│ FOCUS 1.x Native Normalisation │

├──────────┬───────────┬────────────┬────────────────────── ┤

│ Cloud │ Kubernetes│ AI │ Data Platforms │

│ AWS/Az/ │ EKS/AKS/ │ Bedrock / │ Databricks / │

│ GCP/OCI │ GKE/OKE │ OpenAI / │ Snowflake / │

│ │ │ Vertex │ Redshift │

├──────────┴───────────┴────────────┴────────────────────── ┤

│ SaaS · Marketplace · On-Premises DC │

└──────────────────────────────────────────────────────────┘

│

▼

BYOC Secure Relay Proxy

(collector runs inside the customer perimeter —

no billing or usage data ever egresses)

The reason FOCUS 1.x matters as architecture rather than feature is that it is the only way every one of those sources resolves into the same attributable view. A platform that normalises cloud billing but treats Databricks and Snowflake as separate conversations has not solved the regulated CFO’s problem — it has solved 60% of it and left the AI-adjacent data estate, where much of the cost now lives, ungoverned.

How Regulated Enterprises Should Evaluate AI Cloud Economics Platforms {#how-to-evaluate}

The evaluation framework matters more than any feature comparison, because each criterion below silently removes a category of tool that was never designed for a supervised estate. A regulated enterprise should require all seven.

| Evaluation Criterion | Why It Matters in a Regulated Estate |

|---|---|

| Deployment architecture (BYOC) | The cost collector must run inside your perimeter; billing and usage data never egresses. SaaS-only export is a compliance event, not a convenience. |

| FOCUS 1.x native | Every cloud, Kubernetes, and data-platform cost resolves onto the open specification natively — not through a brittle compatibility layer that breaks at the edges. |

| AI workload governance | Token-level attribution, GPU idle detection, agentic kill-switches, and budget caps built in — not retrofitted onto a tool designed for VM costs. |

| Full estate coverage | Cloud + Kubernetes + AI services + Databricks + Snowflake + SaaS + on-premises in one normalised view. Governing 60% of the estate is not governance. |

| Audit-grade attribution | Every cost traceable to a business unit with the evidentiary rigour a supervisor expects — not a dashboard estimate with a 20% unallocated bucket. |

| Flat enterprise licensing | Pricing that does not scale with your cloud bill, so the vendor’s incentive is aligned with your cost reduction, not your spend growth. |

| Regulated-industry proof | Demonstrated deployment at institutional scale under regulatory compliance — evidence the architecture survives contact with a real supervisory environment. |

The commercial criterion deserves emphasis because it is where a structural conflict hides. A platform priced as a percentage of cloud spend earns more as your bill grows — the precise opposite of the incentive a cost-governance tool should have. At a $50M estate, a 3% rate is $1.5M a year; at $100M it is $3M, and the vendor’s revenue rises exactly as your problem does:

What Percentage-of-Spend Pricing Costs at Scale

──────────────────────────────────────────────────────────

Annual cloud spend: $50M

Typical % of spend rate: 3%

Annual platform cost: $1.5M

Annual cloud spend: $100M

Annual platform cost: $3M

──────────────────────────────────────────────────────────

DigiUsher flat enterprise licensing:

Scales with the size of your estate, not the size of your bill.

──────────────────────────────────────────────────────────

For a regulated institution running a multi-year sovereign migration — which McKinsey notes typically takes three to four years, driven by organisational rather than technical limits — a pricing model that compounds against you over that horizon is a strategic liability, not just a line item.

Governing the Full Estate Without Leaving Your Perimeter {#governing-full-estate}

The capabilities that resolve the regulated AI economics problem map directly onto the three constraints established above.

For data sovereignty, the Secure Relay Proxy keeps everything inside the customer’s cloud. The platform reads, normalises onto FOCUS 1.x, and attributes — all within the regulated environment, which is why it is the architecture deployed at a large public listed Bank and why it serves institutions that cannot consider a SaaS-only alternative.

For audit-grade attribution, DigiUsher’s Meter module attributes AI cost at the token, model, team, and environment level, while the platform’s policy layer enforces tagging and allocation rules across cloud, Kubernetes, Databricks, and Snowflake in one view. The European energy utility that identified €1M in savings on its Databricks estate within 45 days did so because the cost finally became attributable, not merely visible.

For defensible ROI and runaway-cost prevention, native AI governance applies token budget caps, GPU idle detection, and agentic kill-switches — controls that stop an unproductive or runaway workload before it compounds into a number someone has to explain. This is the difference between discovering waste in next month’s invoice and preventing it at the moment of consumption.

DigiUsher is SOC 2 Type II certified and GDPR compliant, listed as an AWS ISV Accelerate Partner, Azure ISV Co-Sell Ready, and a GCP Partner, with global enterprise delivery through Infosys, Wipro, and Hexaware. For a regulated buyer, those are not badges — they are the procurement and delivery preconditions that make a sovereign deployment executable.

The Path Forward

The organisations that will report defensible AI returns in 2026 are not the ones that spent the most or the least on AI. They are the ones that instrumented unit economics from the start, inside their own perimeter, so that every token and GPU hour carries a cost identity and an unproductive workload is visible and killable before it becomes a problem.

For regulated industries, that instrumentation has a hard architectural requirement attached: it must run where the data is allowed to live. The economics, the audit, and the board question all converge on the same answer — govern the spend inside the perimeter, on a common specification, with attribution that survives scrutiny.

In regulated industries, the AI cost problem is not that the spend is large. It is that the spend is large, opaque, undefendable to a supervisor, and unreachable by the tools built to govern it. Solving it is an architecture decision before it is an analytics one.

Govern your AI and cloud economics without your data ever leaving your perimeter. Book a 30-minute briefing to see how DigiUsher’s BYOC FinOps Operating System attributes AI spend across your full estate — cloud, Kubernetes, Databricks, Snowflake, and inference — inside your own environment. SOC 2 Type II certified · GDPR compliant · deployed at institutional scale in regulated banking. Request a demo or reach the team at sales@digiusher.com.

Related reading

- The CFO’s Guide to Cloud and AI ROI in 2026 — 2026-04-22 — Turns the board-level ROI argument here into a finance-leader framework for presenting AI returns with audit-grade attribution.

- AI Cost Governance: Bringing GenAI Spend Under Control — 2026-03-18 — Goes deeper on the token attribution, GPU idle detection, and agentic kill-switch mechanics referenced in this briefing.

- The CIO Mandate: Proving Cloud and AI ROI — 2026-02-26 — Covers the reporting-line shift to the CTO/CIO and what that accountability now demands.

- Why a FinOps Operating System, Not Just Another Tool — 2026-01-30 — Explains the full-estate, FOCUS-native architecture the evaluation framework here implicitly requires.

- Azure Landing Zone Cost Guardrails for Regulated Workloads — 2026-01-14 — Applies the data-sovereignty and pre-deployment governance principles here to a concrete regulated Azure pattern.

References

- FinOps Foundation, State of FinOps 2026 — https://data.finops.org/

- MIT Project NANDA, State of AI in Business 2025 (The GenAI Divide) — July 2025

- Gartner, Only 28% of AI Projects Deliver ROI — 2026

- Gartner, Worldwide Sovereign Cloud IaaS Spending Will Total $80 Billion in 2026 — February 2026 — https://www.gartner.com/en/newsroom/press-releases/2026-02-09-gartner-says-worldwide-sovereign-cloud-iaas-spending-will-total-us-dollars-80-billion-in-2026

- Flexera, State of the Cloud 2026 (cloud waste at 29%) — 2026

- Forrester, Public Cloud Market Outlook (public cloud approaching $1.03T in 2026) — 2026

- RAND Corporation, analysis of 2,400+ enterprise AI initiatives (~80% deliver no measurable value) — 2025

- McKinsey & Company, Sovereign AI: Building Ecosystems for Strategic Resilience and Impact — March 2026 — https://www.mckinsey.com/industries/technology-media-and-telecommunications/our-insights/sovereign-ai-building-ecosystems-for-strategic-resilience-and-impact

- CIO Dive, FinOps Teams Gain Clout as AI Costs Climb — February 2026 — https://www.ciodive.com/news/finops-teams-gain-clout-ai-costs-climb/812887/

- Kiteworks, AI Governance Solutions for Regulated Industries (54% rank AI governance a top risk) — 2026 — https://www.kiteworks.com/cybersecurity-risk-management/ai-governance-solutions-regulated-industries/

DigiUsher in 30 min

Your regulated AI workloads deserve attribution that survives an audit.

DigiUsher maps every workload to an owner and a policy — so compliance reviews start from evidence, not spreadsheets.

Book a 30-min walkthroughNo hard pitch · tailored to your stack

Continue Reading

More from the DigiUsher editorial team.

Why Your FinOps Team Needs a Dedicated Cloud Cost Analyst in 2026

Explores the emerging role of specialized cloud cost analysts and how they differ from traditional financial analysts in driving FinOps success

AKS vs EKS vs GKE vs On-Prem vs OpenShift: Cost Governance Deep Dive

Not all Kubernetes platforms are economically equal. This FinOps deep dive compares AKS, EKS, GKE, on-prem Kubernetes, and OpenShift across cost visibility, pricing structure, optimisation potential, and governance capability — with a practical framework for making Kubernetes platform economics a competitive advantage in 2026.

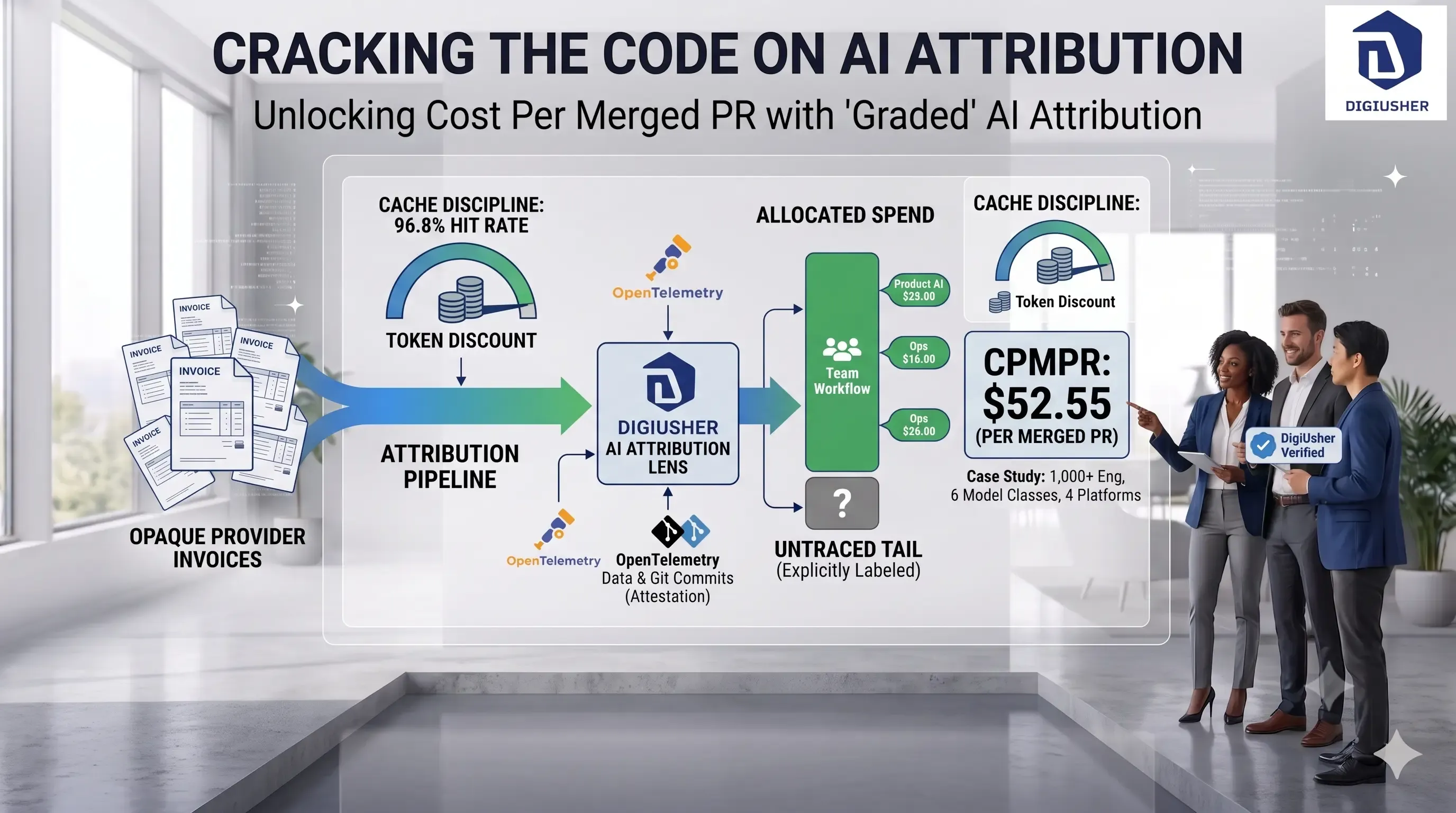

$52.55 Per Merged Pull Request: How One 1,000-Engineer Firm Priced Its Own AI Spend

A public technology firm with 1,000+ engineers refused to run its AI spend on faith. Here's the ledger it built instead — $52.55 per merged PR, 96.8% cache-hit rate, and a blended cost of $0.75 per million tokens.