The Silent Transformation of Enterprise Cloud Buying

Enterprise software sales through cloud marketplaces will grow from $30 billion in 2024 to $163 billion by 2030. Cloud procurement is no longer a sourcing function — it has become a continuous financial operations discipline. This briefing explains the three forces reshaping enterprise cloud buying, why the CIO and CFO must act together, and what it means when FinOps shifts up from cost reporting to board-level technology investment strategy.

Executive Summary

Enterprise cloud procurement is undergoing one of the most consequential structural shifts since the birth of hyperscale infrastructure — and it is happening quietly, one private offer at a time.

For more than a decade, organisations purchased software through fragmented channels: direct vendor contracts, reseller agreements, and procurement-heavy enterprise licensing negotiations that consumed months and required legal, finance, and IT sign-off at every step.

That model has not evolved. It has been displaced.

Cloud marketplaces — AWS Marketplace, Azure Marketplace, Google Cloud Marketplace — have emerged as the primary commercial layer for enterprise technology consumption. And the data reveals a transformation that is accelerating, not stabilising:

- Enterprise software sales through cloud marketplaces will grow from $30 billion in 2024 to $163 billion by 2030 — a more than five-fold increase in six years (Omdia)

- $470 billion in enterprise cloud commitments across AWS, Azure, and Google Cloud now serve as the primary enterprise buying budget

- 64% of organisations now measure cloud progress by value delivered to business units — up 12 percentage points in one year, the single largest shift in cloud KPI measurement ever recorded (Flexera 2026)

- By 2030, 60% of all marketplace transactions will be channel-partner-facilitated — GSIs and partners evolving into commercial orchestrators inside hyperscaler ecosystems (Omdia)

“Cloud has entered a new era — one defined less by infrastructure decisions and more by the clarity, confidence and value organisations expect from every technology investment.” — Flexera 2026 State of the Cloud Report

This transformation has a governance consequence that most enterprises are not yet equipped for: the speed of cloud-native procurement has dramatically outpaced the financial governance infrastructure designed to account for it.

This briefing explains the three structural forces reshaping enterprise cloud buying, the strategic shift in FinOps that this change demands, and what CIOs and CFOs must do together to govern technology procurement in the marketplace era.

The Magnitude of the Shift

The numbers behind the cloud marketplace transformation are not incremental. They describe a categorical change in how enterprise technology is financed, distributed, and governed.

Cloud Marketplace Growth Trajectory (Omdia, 2026)

──────────────────────────────────────────────────────────

2024 $30B in enterprise software marketplace sales

2026 $60B+ AI marketplace opportunity alone (S&P Global)

2030 $163B total enterprise marketplace transactions

↑ 5.4× in six years

──────────────────────────────────────────────────────────

Channel facilitation: ~40% of marketplace transactions today

60% by 2030 (Omdia)

──────────────────────────────────────────────────────────

Committed pool: ~$470B across AWS, Azure, GCP

The budget that marketplace draws against

──────────────────────────────────────────────────────────

The contextual reality behind these numbers: 76% of large enterprises now spend more than $5 million monthly on public cloud (Flexera 2026). For these organisations, the cloud bill has become the primary technology P&L — and marketplace procurement is increasingly the mechanism by which that P&L is populated.

The IDC MarketScape positioned Google as a Leader in the 2025 assessment of Worldwide Hyperscaler Marketplaces — recognising strategic investment in AI agent distribution, agentic and generative AI solution portfolios, and governance tooling for enterprise procurement. All three hyperscalers are investing at comparable scale in marketplace as the primary enterprise commercial infrastructure of the AI era.

The Three Forces Reshaping Enterprise Cloud Buying

Force 1 — Cloud Commitments Are Becoming the Enterprise Buying Budget

Enterprises have accumulated $470 billion in committed cloud spend across AWS, Azure, and Google Cloud. These multi-year agreements were originally structured around infrastructure consumption. Cloud-native procurement has transformed them into a universal enterprise buying budget.

How it works: software vendors list products on hyperscaler marketplaces. Enterprises purchase through the marketplace using existing committed spend — with transactions appearing on the cloud invoice and counting toward committed consumption thresholds. SaaS and AI procurement becomes committed cloud consumption, financed from existing budget approvals without new capital cycles.

Why CFOs cannot ignore it: cloud commitment strategy and marketplace procurement strategy are now the same financial decision. A CFO managing $50M in annual cloud commitments across AWS, Azure, and GCP is simultaneously managing the enterprise’s primary technology buying budget. Marketplace procurement decisions that burn committed capacity inefficiently — through incorrect credit rate assumptions, duplicate SaaS purchases, or ungoverned AI consumption — erode the ROI of the commitment structure itself.

McKinsey’s 2026 technology investment analysis confirms: organisations that align cloud commitment strategy with marketplace procurement governance achieve measurably better technology investment ROI than those treating the two as separate disciplines. Cloud spend is no longer an operational IT cost. It is a strategic capital allocation decision — and the CFO must own it accordingly.

Force 2 — AI Is Choosing Marketplaces as Its Primary Distribution Channel

S&P Global frames cloud marketplaces as AI’s “predominant distribution network.” The AI marketplace opportunity is sized at $60 billion for 2026 alone. AI vendors — model providers, inference platforms, AI agent frameworks, AI data services — are defaulting to hyperscaler marketplace distribution rather than building independent enterprise sales channels.

The reason is structural: enterprise buyers have already committed cloud budgets. Purchasing AI from an existing committed cloud pool requires no new procurement cycle, no new legal engagement, and no new billing integration. The commercial friction that used to gate AI adoption has been eliminated by marketplace infrastructure.

The governance consequence is significant. When AI services are purchased through marketplace channels, the billing abstraction compounds:

AI through Marketplace — The Attribution Stack

──────────────────────────────────────────────────

Layer Cost Event

──────────────────────────────────────────────────

GPU hardware NVIDIA silicon cost (invisible)

Cloud infra AWS/Azure/GCP CapEx recovered

AI platform Bedrock / Azure OpenAI / Vertex

Model provider Token pricing per API call

Marketplace Transaction billing to enterprise

──────────────────────────────────────────────────

Enterprise invoice: One marketplace line item

Attribution: None without external tooling

──────────────────────────────────────────────────

The AI infrastructure reckoning — named as such by IDC FutureScape 2026 — is partly a marketplace governance problem. IDC warns that G1000 organisations face up to a 30% rise in underestimated AI infrastructure costs by 2027 — not from reckless spending, but from the structural failure to attribute costs that arrive as consolidated marketplace charges to the AI workloads and teams generating them.

The agentic escalation. IDC projects enterprises will be managing more than 2 billion AI agents by the end of 2026 — 80 times the 28.8 million deployed in 2025. Each agent accessing AI services through marketplace channels represents both a procurement event and a continuous financial governance requirement. As one cloud economist put it at the Gartner Data & Analytics Summit in March 2026:

“An agent doesn’t know it’s bankrupting you; it just thinks it hasn’t found the answer yet. Without a governance intelligence layer to throttle these cycles, your ROI evaporates before the first dashboard even refreshes.”

The implication: AI marketplace governance is not a future capability need. It is a present operational requirement for any enterprise deploying AI agents at scale.

Force 3 — Channel Partners Are Becoming Commercial Orchestrators

For forty years, Global System Integrators built value by implementing and integrating enterprise technology. In the marketplace era, they are building value by structuring commercial transactions — attaching service margin within a single hyperscaler billing event rather than billing separately for consulting and system integration.

The mechanism: AWS Channel Partner Private Offers, Microsoft Multiparty Private Offers (MPO), and Google Cloud Channel Services Private Offers each provide the commercial infrastructure for partner-to-partner commerce inside marketplace ecosystems. A Microsoft MPO enables a GSI to participate commercially in an ISV transaction — attaching service fees, structuring deal economics, and creating a single enterprise purchase that covers software, services, and commercial support.

By 2030, Omdia projects 60% of all marketplace transactions will be channel-partner-facilitated. The implications for enterprise buyers are dual:

Commercial efficiency gain: partners absorb deal structuring complexity. Enterprise procurement moves from managing fifteen vendor relationships to managing three marketplace channels, each orchestrated by trusted partners with deep commercial expertise.

Financial governance requirement: partner margins are embedded in commercial transactions that appear as single marketplace line items. The ISV cost, the GSI service margin, the hyperscaler platform fee — consolidated into one billing event with no native disaggregation. Without financial governance tooling that can map contracted private offer terms to billing actuals, enterprise buyers cannot verify whether partner-orchestrated deals are delivering the negotiated economics.

The FinOps Shift Up: From Cost Reporting to Technology Investment Intelligence

The three forces transforming cloud procurement are simultaneously transforming what FinOps teams are expected to do. The FinOps Foundation documented this evolution formally in its 2026 Framework update — describing a discipline that is shifting both left (earlier in the delivery lifecycle) and up (into board-level technology investment strategy).

The 2026 State of FinOps data tells the structural story:

| Dimension | 2023 FinOps Model | 2026 FinOps Model |

|---|---|---|

| Primary output | Monthly cost reports | Technology investment ROI |

| Scope | Public cloud infrastructure | Cloud + SaaS + AI + Marketplace + Licensing |

| Success metric | Cost saved | Value delivered to business |

| Executive relationship | Reports to VP Finance | 4 in 5 FinOps teams report to CIO |

| Procurement involvement | None | Provider negotiations, commitment modelling |

| AI role | Not in scope | Top priority and top tooling gap |

Source: FinOps Foundation State of FinOps 2026 / Flexera 2026 State of the Cloud Report

The “shift up” in practice: FinOps leaders are now participating in provider negotiations, multi-year commitment modelling, and M&A diligence discussions. They are answering ROI and investment realisation questions at board level — not producing retrospective cost reports for engineering teams to ignore.

“FinOps is becoming a decision-support system for enterprise technology strategy. Financial governance and operational governance are no longer separate conversations.” — theCUBE Research, FinOps 2026 Analysis

The FinOps Foundation reflected this in its most significant statement of institutional direction in the discipline’s history: the Foundation formally updated its mission from managing “the value of cloud” to managing “the value of technology.” The scope expansion is not aspirational — it reflects the operational reality that 2026’s FinOps teams are already governing: cloud, SaaS, AI, marketplace transactions, private cloud, on-premises, and data centre.

This is what the FinOps Foundation calls FinOps Cloud+: the full technology cost surface, governed by a unified financial operating model.

From Vendor Contracts to Cloud-Native Procurement: The Full Transition

The transformation of enterprise cloud buying is best understood not as a linear evolution but as a complete model replacement — one that has already happened for most large enterprises, whether their governance models recognise it or not.

| Attribute | Legacy Model | Cloud-Native Procurement |

|---|---|---|

| Channel | Direct vendor contracts | Hyperscaler marketplace private offers |

| Pricing model | Annual licensing — static, predictable | Consumption economics — usage-based, commit-aligned |

| Deal cycle | 6–9 months (legal, procurement, IT) | Days to weeks (marketplace standardisation) |

| Financial owner | Procurement team | FinOps team |

| Agreement type | Static contracts, periodically renewed | Dynamic commercial optimisation, continuously governed |

| AI procurement | Separate vendor contract, IT-managed | Marketplace-distributed, commit-financed, FinOps-governed |

| Partner role | Technology implementer | Commercial orchestrator |

| Billing unit | Vendor invoice, separately attributed | Cloud invoice, consolidated, partially attributed |

| Success metric | Contract value, vendor relationship | Business outcome ROI, commitment utilisation |

The transition is not complete. Most enterprises are operating with legacy governance models applied to a cloud-native procurement reality — generating the exact financial opacity that the marketplace era has introduced. Organisations that fail to govern marketplace spend are not facing a gradually worsening problem. They are facing structural financial unpredictability that compounds at the rate of marketplace adoption.

What the CIO and CFO Must Do Together

The transformation of enterprise cloud buying requires joint action from the two executive roles most affected — because the financial governance of marketplace procurement sits at the intersection of technology strategy (CIO) and capital allocation accountability (CFO).

Unify commitment strategy with marketplace procurement governance. The $470 billion in enterprise cloud commitments is a shared CIO/CFO accountability. Commitment decisions made without visibility into how marketplace procurement will draw against them are capital allocation decisions made with incomplete information. A jointly owned commitment and marketplace governance model is no longer optional at large-enterprise scale.

Elevate FinOps to technology investment intelligence. The enterprises where FinOps teams have CIO-level sponsorship show dramatically greater influence over technology selection decisions than those where FinOps reports to VP Finance. This is not an organisational preference — it is a governance design requirement. FinOps teams that can participate in commitment modelling, provider negotiations, and AI investment decisions before spend is committed prevent the governance failures that no retrospective reporting can fix.

Govern AI procurement before agents govern it for you. By the end of 2026, enterprises will be managing more than 2 billion AI agents — each accessing AI services through marketplace channels and generating continuous inference costs against committed cloud budgets. The FinOps Foundation’s 2026 analysis explicitly flags AI agent proliferation as a shadow IT risk: “I’m worried that shadow IT is coming back with a vengeance when it comes to these AI agents and how easy they’re going to be to create.” Agent inventory management, token budget governance, and automated kill-switch infrastructure for runaway inference costs are not advanced FinOps capabilities. They are table-stakes requirements for any enterprise deploying AI at scale in 2026.

Measure technology by value, not cost. 64% of organisations now measure cloud progress by value delivered to business units. The remaining 36% are applying a cost-reduction KPI framework to technology investments generating AI-driven competitive advantages — a measurement approach that systematically undervalues transformation and overstates cost as the primary governance variable. CIOs and CFOs who align on value-delivered metrics for technology investment decisions are building the financial accountability model that the marketplace era requires.

DigiUsher: The Operating Model for Cloud-Native Procurement

DigiUsher’s FinOps Operating System is built for the commercial architecture that cloud-native procurement has created — where every element of enterprise technology acquisition flows through hyperscaler billing and demands the same continuous financial governance that cloud infrastructure has always required, at greater scale and higher velocity.

FOCUS 1.x unified attribution — all cloud, marketplace, SaaS, AI, and partner service costs normalised to a single cost model. The cross-domain financial view that turns a three-invoice fragmentation problem into one source of governance truth.

Commitment intelligence — real-time commitment utilisation tracking with credit rate awareness across AWS, Azure, and GCP. The CFO dashboard that answers whether committed capital is being deployed at the expected rate — across every marketplace channel simultaneously.

AI and agent governance — token budget enforcement, agent inventory management, and automated kill-switch infrastructure for AI services purchased through marketplace channels. Governance that acts at the speed of autonomous procurement, not the cadence of monthly billing reviews.

Technology value measurement — cost-per-business-outcome metrics connecting every marketplace transaction to the product, team, and strategic initiative it serves. The board-ready ROI intelligence that transforms FinOps from cost reporter to technology investment strategist.

Private offer ROI validation — contracted partner deal terms mapped to billing actuals. The commercial intelligence that answers whether channel-orchestrated marketplace deals are delivering the negotiated economics.

Available as SaaS or BYOC for regulated industries. SOC 2® Type II and GDPR certified. Delivered globally through Infosys, Wipro, and Hexaware. AWS ISV Accelerate Partner listed on AWS Marketplace.

The winners in the cloud marketplace era will not be those who purchase fastest. They will be those who govern consumption most intelligently — connecting every marketplace transaction to the business outcome it funds, in real time, at the speed that cloud-native procurement demands.

Frequently Asked Questions

What is transforming enterprise cloud buying in 2026 and why does it matter for CIOs and CFOs?

Three structural forces: $470 billion in cloud commitments becoming the enterprise buying budget; AI vendors adopting marketplaces as their primary distribution channel ($60B opportunity in 2026); and channel partners becoming commercial orchestrators (60% of marketplace transactions channel-facilitated by 2030). For CIOs, technology procurement strategy and cloud commitment strategy are the same decision. For CFOs, the cloud bill now finances most enterprise technology acquisition — and commitment ROI is now a board-level governance question.

What is FinOps Cloud+ and how does it differ from traditional cloud FinOps?

FinOps Cloud+ is the formal expansion of FinOps scope beyond public cloud to encompass SaaS, AI services, licensing, private cloud, marketplace transactions, and data centre infrastructure. The FinOps Foundation formalised this in its 2026 Framework update by changing its mission from managing “the value of cloud” to managing “the value of technology.” In practice: cloud cost governance plus marketplace attribution, AI token governance, SaaS lifecycle management, and partner commercial analytics in one unified operating model.

What is cloud-native procurement and how should FinOps teams govern it?

Cloud-native procurement is the enterprise model where software, AI, and partner services are transacted through hyperscaler marketplace environments and drawn against committed cloud budgets. FinOps governance requires: unified attribution mapping every marketplace transaction to owning teams and outcomes; commitment tracking with platform-specific credit rate intelligence; spend classification separating SaaS, AI, and infrastructure within the cloud bill; private offer ROI validation; and AI marketplace governance connecting billing to token consumption.

How are AI agents changing the cloud procurement governance challenge?

IDC projects enterprises will manage 80× more AI agents by year-end 2026 than were deployed in 2025. Each agent accessing AI services through marketplace channels is a continuous procurement event generating inference costs against committed cloud spend. Without agent inventory management, token budgets, and automated kill-switch infrastructure, autonomous procurement at 2 billion-agent scale generates the same governance failures as Shadow IT — at machine speed and AI cost levels.

What does the FinOps “shift up” mean for enterprise technology strategy?

FinOps leaders are now participating in cloud provider negotiations, multi-year commitment modelling, and M&A diligence. Nearly 4 in 5 FinOps teams report to the CIO. The FinOps Foundation updated its mission from cloud cost management to technology value management. This means FinOps is no longer a finance-adjacent IT function — it is a technology investment intelligence layer that informs capital allocation decisions at board level.

How does DigiUsher support the transformation to cloud-native procurement?

Through five integrated capabilities: FOCUS 1.x cross-marketplace normalisation; commitment intelligence with platform-specific credit rate awareness; AI and agent governance with token budgets and kill-switch infrastructure; technology value measurement connecting every transaction to business outcomes; and private offer ROI validation ensuring partner-orchestrated deals deliver contracted economics.

References

- Omdia / CIO Dive — Enterprise Cloud Marketplace Sales: $30B to $163B by 2030

- Flexera — 2026 State of the Cloud Report: Value Era Begins

- FinOps Foundation — State of FinOps 2026

- FinOps Foundation — 2026 FinOps Framework Update: FinOps Cloud+

- IDC — Balancing AI Innovation and Cost: The New FinOps Mandate

- Google Cloud Blog — IDC MarketScape: Worldwide Hyperscaler Marketplaces 2025 Leader

- theCUBE Research — FinOps 2026: Shift Left and Up as AI Drives Technology Value

- CIO Dive — AI Spend Management: CIOs and FinOps Teams (FinOps Forward 2026)

- Clazar — Cloud Marketplace Partner Trends 2025–2026

- AnalyticsWeek — The $400M Cloud Leak: FinOps Reckoning for Agentic AI 2026

- Intellectt — Cloud Cost Optimisation 2026: AI-Driven FinOps

- S&P Global — Marketplaces as AI’s Predominant Distribution Network

- Morningstar / Cyberhaven — Enterprise Cloud Marketplace Procurement, April 2026

- FinOps Foundation — FOCUS Specification

The New Enterprise Buying Model Demands New Financial Governance

Cloud-native procurement is not a future state — it is the present operating reality for enterprises with meaningful cloud commitments. The $470 billion already committed is being deployed through marketplace channels, by channel partners, for AI services, at a speed that legacy governance models were never designed to govern.

DigiUsher’s FinOps OS provides the unified intelligence layer that connects marketplace commercial speed to financial accountability — normalising procurement events from all three hyperscalers into a single attributed governance model, in real time.

DigiUsher in 30 min

Give your board a cost-to-outcome view they can actually act on.

DigiUsher connects cloud and AI spend to the outcomes it funds, in language finance already speaks.

Book a 30-min walkthroughNo hard pitch · tailored to your stack

Continue Reading

More from the DigiUsher editorial team.

Board-Level Cloud and Data Centre ROI: Governing the Full Technology Estate in 2026

Cloud waste runs at 29-35% of spend. GPU idle time hits 30-60%. Data centre costs surpass $650B in 2026. Here is the board-level governance framework that connects every infrastructure dollar to measurable business value.

Why FinOps Is Now a Board-Level Responsibility

FinOps has moved from cloud cost control to enterprise value governance. Only 15% of AI decision-makers report an EBITDA lift from AI investment. Fewer than one in three can tie AI spend to P&L outcomes. This briefing explains the structural forces making FinOps a board-level discipline in 2026 — and what the CFO-CIO convergence requires of every enterprise managing cloud and AI at scale.

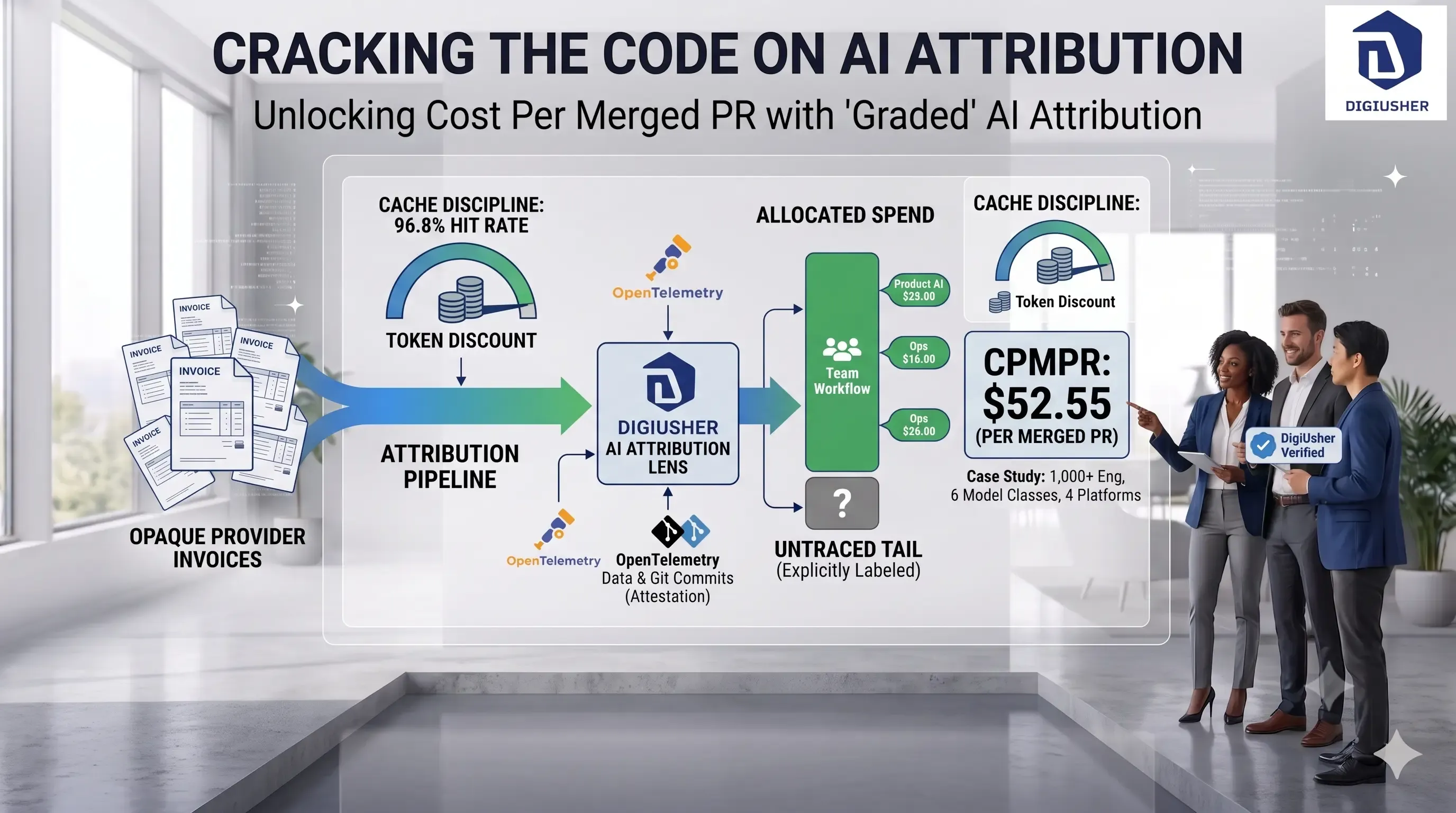

$52.55 Per Merged Pull Request: How One 1,000-Engineer Firm Priced Its Own AI Spend

A public technology firm with 1,000+ engineers refused to run its AI spend on faith. Here's the ledger it built instead — $52.55 per merged PR, 96.8% cache-hit rate, and a blended cost of $0.75 per million tokens.